This post may contain affiliate links. As an Amazon Associate I may earn from qualifying purchases at no additional costs to you. Please see the Policies pages for more info.

How to Make a Budget for Beginners

Have you ever asked yourself a day or two before payday, “where did all my money go?” It’s probably because you don’t have a written budget for it. As financial guru Dave Ramsey would say, “A budget is telling your money where to go instead of wondering where it went. You are putting a name to every dollar before you spend it.”

“Putting a name to every dollar” is done with a zero-based budget. A zero-based budget is when your monthly income minus your monthly expenses equals zero. This does not mean you drain your bank account to zero each month. It’s simply allocating your income so you know how to cover all your expenses. It doesn’t have to be a complicated task. Here are 5 simple steps to get started on your budget.

What is a Zero-Based Budget?

I am going to go over how to set up a zero-based budget. A zero-based budget means monthly income less monthly expenses equals zero. It’s planning your expenses for the month based on your income. I will share the categories to prioritize and how to adjust if your number doesn’t equal zero.

1. Best Place For Your Budget

First, decide where you would like to have your budget. Are you a paper or digital person? It doesn’t matter which one you choose, just choose something that works for you. You can also have a combination of both of that works as well.

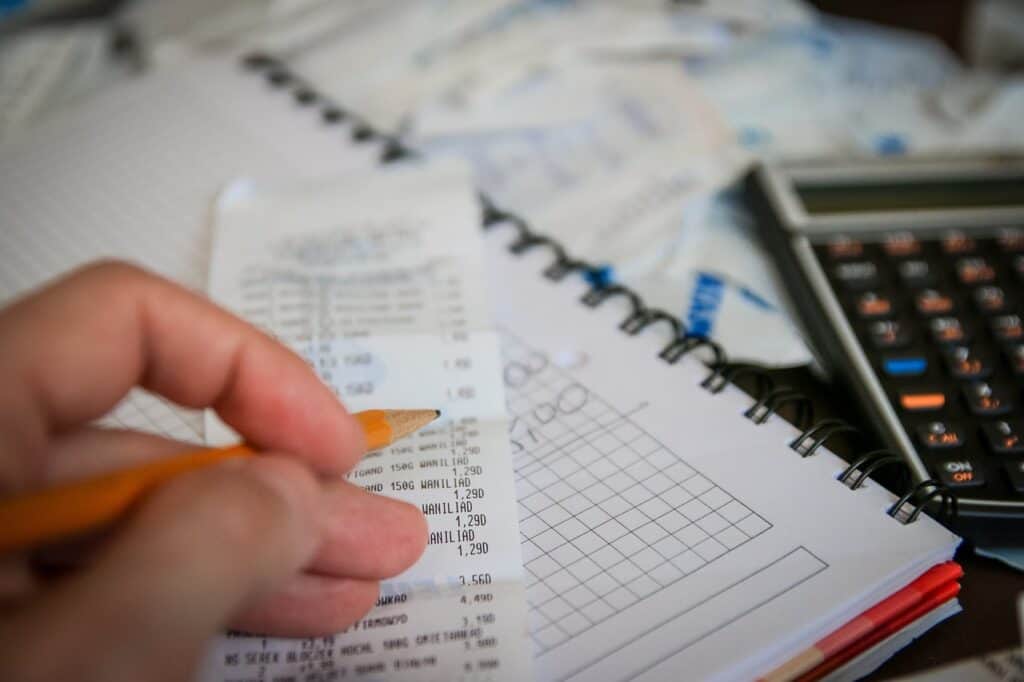

Budgeting on Paper

Setting up your budget on paper can be as simple as using a lined notebook or having a budgeting worksheet or planner. Whichever method you use, there should be 4 columns. Here is an example:

| Categories | Budget | Actual | Difference |

The first column is categories, this is where you list all your income and expenses for the month (more on that in the following steps). The second column is the budget column, where you will list out your expected income and expenses for the month.

The actual is updated throughout the month where you will track your income and expenses. The Difference column is difference between budget and actual (Budget – Actual). This will show you if you are over or under budget in that area.

If you are a pen to paper type person or lover of planners this might work best for you. This is a nice simple budget planner that might work for you.

Using a Budgeting Spreadsheet

If you prefer electronic methods over paper there are several easy platforms you can use. Microsoft Excel and Google Sheets have budgeting templates. We used a budgeting template from Google Sheets for years before we started using an app.

You can always create your own spreadsheet as well.

Budgeting Apps

EveryDollar is my favorite app for creating our budget each month. You can create your budget on the website or through the app on your phone. To start an account you only need one email and password to sign in but multiple users can use it. This is helpful for couples.

There is a free version and a paid version. You can create your whole budget with the free version, you will just have to enter each transaction in manually.

With the paid version you will have the ability to link your bank accounts. This will feed your transactions into EveryDollar so then all you have to do is categorize those transactions to update your budget. Easy peasy!

2. Write Down Monthly Income

Once you have decided if you would like to use paper or digital, the next step is to list your monthly income. This is all monthly take home income, including your spouse’s paycheck, part time jobs and child support. This is your starting point and the number you get to work with before listing expenses.

3. Cover Your 4 Walls

With any budget you will want to make sure you are covering your basic needs first or your “4 walls.” The 4 walls include:

- Food

- Shelter (rent, mortgage, insurance)

- Utilities (electric, water, gas)

- Transportation (gas, insurance, car payment)

These categories should be prioritized above everything else. Taking care of your family is more important than paying creditors.

4. List Other Expenses

After you have budgeted for your 4 walls, list out your other expenses. I find it easier to do the ones that are pretty much the same each month first – these are fixed expenses. Fixed expenses include debt payments, savings, giving, tv, internet, phone, subscriptions, etc.

Once you have the fixed expenses listed then include other variable categories such as clothing, household supplies, gas for your vehicle, special events, etc.

Don’t forget to include personal spending money for each adult in the house. Personal spending category gives that person the freedom to spend their money how they wish without guilt.

5. Adjust As Needed and Update Regularly

As you go through each category, make sure your total expenses are equal to your total income – that is a zero-based budget! If they don’t match up you will have look at each category and see how it can be adjusted.

Once your budget is set, update your actual income and expenses regularly throughout the month. You will want to do this daily or weekly so you can compare your actual income and expenses to what you planned for.

Tracking your spending is the important part about budgeting. Just making a budget at the beginning of the month is not helpful if you are not paying attention to what you are spending.

Also know that what you planned for at the beginning of the month won’t be 100% accurate as the month goes on. Your budget is not set in stone. If you end up spending more in one category that just means you will have to adjust another category so you are not spending more than you earn.

A good example of a fluctuating cost is gas prices. You can do you best guess on how much you plan to spend but if you end up driving more or prices go up then you may spend more than planned. That’s ok! For these types of expenses you may want to over calculate on what you think you will spend to give yourself some margin.

Stay the Course

If budgeting is new to you then this might feel frustrating at times but stay the course! It can take about 90 days to get in the habit and identify spending patterns.

Making a plan for your money each month is the foundation to all your financial goals and financial wellness. Start making a plan for your money today. Give yourself grace – it doesn’t have to be perfect.

Comment below – how have you tried budgeting in the past? What has been your biggest challenge?

Related Articles to Help You With Your Budget

How the Zero-Based Budget Can Provide Money Confidence

Organize Your Money With These Common Budget Categories

How to Budget While Living Paycheck to Paycheck

How to Set Short Term Financial Goals